I’m planning to do monthly updates on my progress to financial independence. If nothing else, it will be an awesome way to look back on the journey in the future. I’ll also be able to look back on the change in value of my investments each month. I only recently began to experiment with Excel so I am by no means an expert with the graphs that are produced but I’ll do my best.

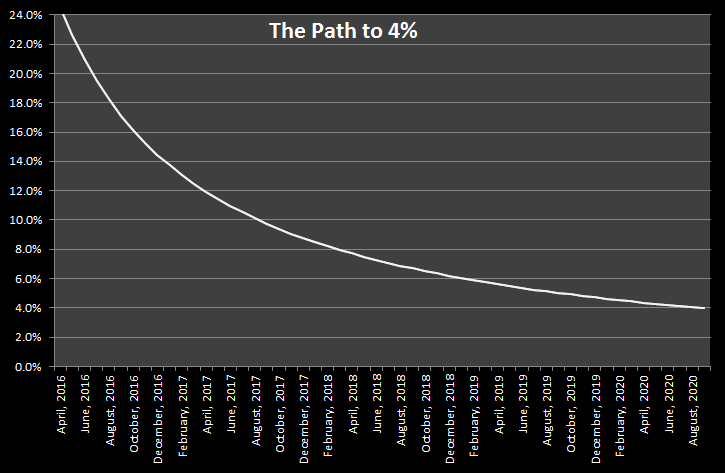

For the time being, I am going to avoid posting specific numbers but I may reveal more specifics later but I haven’t decided yet. It feels a little personal and unsafe to me to discuss my exact net worth and expenses in dollar amounts. Instead of specific numbers, I will track my progress to financial independence based on the “4% rule.” It you are unfamiliar with this concept, I will be publishing a post about it in the very near future. It basically states that, in a well diversified portfolio, you will be able to withdraw 4% of your net worth every year and never run out of money. This means that when my yearly expenses are 4% or less of my net worth, then I will consider myself financially independent. Here is a graph of how I estimate that my progress to 4% will look over the next four and half years.

As you can see on this graph, my current yearly expenses are approximately 24% of my net worth as of today. This means that I have quite a ways to go in order to get to that safe withdrawal rate of 4%. Since I have only been out of school for less than a year at this point, I feel that my progress has been pretty good so far. I could technically take at least 4 years off of work and not run out of money as long as I continued my current spending each month. That’s exciting for me to think about but not even close to the ultimate goal.

The really exciting part is on the right side of the graph. This shows that I should reach my financial independence goal around September, 2020. In reality, that is not that far away. If that estimate holds up, that will mean that it will have only taken five years and three months of working, after finishing school to reach financial independence. Pretty crazy, right?

Now, let me explain some of the assumptions that I used to create this graph. I’m estimating an average growth rate of 6% per year of my investment portfolio. Over the history of the stock market, this would be considered a conservative estimate but I believe that with the current valuations in the market it is probably realistic. I assume that my savings rate will be, on average, a little less than it has been over the past year. This is because I have been working overtime most of this year, as well as making extra money working a PRN job and completing credit card, bank account, and brokerage account sign-up bonuses. I don’t expect to be able to continue this for the next four and a half years, at least not to the same extent, so I estimated a little lower. I also estimated that my expenses will increase about 25% over time, especially since I plan to eventually have kids. If the numbers were based on my current expenses, I would be reaching the goal much sooner.

I am optimistic that my projections are conservative and that I will actually be able to reach financial independence sooner than September, 2020 but I would rather be more conservative since the future is unknown. I’m going to work as hard as I can to be able to get to the goal three months earlier so that I will be able to say that my “working career” was only five years. That sounds pretty awesome in my opinion. What do you guys think? How long until you reach FI?

Excellent plan, man. My current projections put us at FI when I’m about 45; I turn 30 later this year. I don’t necessarily see myself ever fully retiring, instead doing PRN work and thereby decreasing the necessary nest egg to “retire.” Another option would be to take a three month travel gig and then essentially retire the other nine months of the year and, if desired or necessary, pick up a little PRN work during that time. So many options, all with the potential to drastically shorten my full-time working career. So maybe 45 will be more like 38-40? Isn’t healthcare such an incredible career field? 🙂

LikeLiked by 1 person

Awesome! My current projections put me at financial independence just before I turn 33. With that being said, I agree with you and I will likely never really “retire” but I may choose to go back to school for something else or continue to work PRN. I have also considered the one travel assignment a year idea but I feel that I would get rusty in the nine months off and be nervous and anxious about going back to work so I likely won’t go that route. Working in healthcare is very helpful because there are so many options for work.

LikeLiked by 1 person

That’s incredible; congratulations on your hard work! Turning 30 later this year, I can’t even imagine how incredible it must feel to know that. So many “if only…” scenarios and thoughts to ponder. Hindsight will always be 20/20, ya know?

I’ve had someone else voice the same concern about getting rusty by doing that but, while I totally respect the idea of it, I don’t really fear it. So long as you maintain proper certifications, licenses, etc. and stay up-to-date on CEU’s and evidence-based practice stuff, I don’t personally see it being an issue. Speaking from the nursing standpoint, the patient-care aspect of nursing remains relatively unchanged…it’s all about being able to utilize the resources at your disposal (e.g. med reference books and policy/procedure document) to ensure patient safety.

No matter what I ultimately decide is my best option, it’s like you said, healthcare provides so many different options and avenues to take. It’s what drew me to nursing: thousands of different career paths, ranging from hospital settings, clinical research, academia, consulting…and the list goes on.

LikeLiked by 1 person

Looking forward to seeing you progress! – Mrs. FE

LikeLiked by 1 person

Wow that’s fast! You must have a very impressive savings rate. 75-80%?

Especially with the option to work for 3 months a year you should be in very good shape, just in case there is a drawdown in the stock market during retirement.

LikeLiked by 1 person

Thanks! I just started working full time at the end of June last year. The other night I calculated my savings rate for the last half of 2015 and it was around 89.5%. This amount included some overtime, credit card cashback bonuses, bank account bonuses, as well as extra money buying and selling gift cards. Also that included a very low cost of living while on my first few travel assignments in Virginia. I won’t be able to save at that rate this year but I’m still optimistic that it will be over 80%. I’ll likely continue to work part time even after FI just because I enjoy my job and helping people is rewarding. A three month travel assignment once a year would more than cover my expenses but I worry about becoming rusty with my skills in the nine months off.

LikeLike